Bonds 101: A Beginner’s Primer

You likely have bonds in your portfolio, but do you understand how they work? This should help.

Most investors are familiar with the stock market. It’s where headlines are made and fortunes rise and fall. But there’s another market — quieter, larger, and often misunderstood — that plays just as important a role in investing and finance: the bond market.

I’ll admit that early in my investing journey, I didn’t pay much attention to bonds. I knew they were less volatile than stocks and didn’t grow as much, but that was about it. Like many investors, I favored the excitement (and growth potential) of equities. It wasn’t until I took a graduate finance course that I really grasped how bonds worked and why they matter.

If you’ve ever wondered whether you really understand bonds, this primer is for you.

What Is a Bond?

At its simplest, a bond is a loan. When you buy a bond, you’re lending money to a government or company (the issuer). In return, they promise to pay you interest (the coupon rate) at regular intervals and then return your principal (the par value) when the bond matures.

Think of a bond as an IOU. Historically, these came with physical certificates. Today, they’re electronic, but the concept is the same: a contract with value that can be traded.

Key Terms You Need to Know

Understanding a few core terms makes bonds much less intimidating:

Coupon Rate – The interest rate the issuer pays, usually semiannually, though sometimes monthly, quarterly, or annually.

Par Value (Face Value) – The amount you’ve loaned, typically $1,000 per bond. This is repaid at maturity.

Maturity Date – The exact date when the issuer must repay your principal.

Maturity (Term) – The length of time from issuance to maturity (e.g., a “10-year Treasury”).

Credit Rating – A grade assigned by agencies like Moody’s or S&P that indicates the issuer’s ability to repay. AAA is the safest; D means default.

These terms form the foundation for understanding all the different flavors of bonds.

Why Do Governments and Corporations Issue Bonds?

Every organization needs money to operate. Ideally, a business funds itself entirely through revenue, but that’s rarely enough. Growth requires additional capital, and even governments need to borrow.

There are two main ways to raise money:

Debt Financing – Borrowing through loans or bonds. This creates an obligation to pay interest and repay principal.

Equity Financing – Selling ownership stakes (stock). Investors share in profits but also dilute the founder’s control.

Debt financing has the advantage of preserving ownership, but it comes with the stress of required payments. Equity financing avoids fixed obligations but gives up control and future profits. Bonds let governments and companies tap into the debt markets at scale, and let investors like us earn interest.

How Big Is the Bond Market?

Here’s a surprising fact: the bond market is actually larger than the stock market.

Globally: about $135–140 trillion in bonds vs. $110–120 trillion in equities.

In the U.S.: about $50–55 trillion in bonds vs. $45–50 trillion in stocks.

So, while bonds don’t grab the same headlines as stocks, they’re the backbone of global finance.

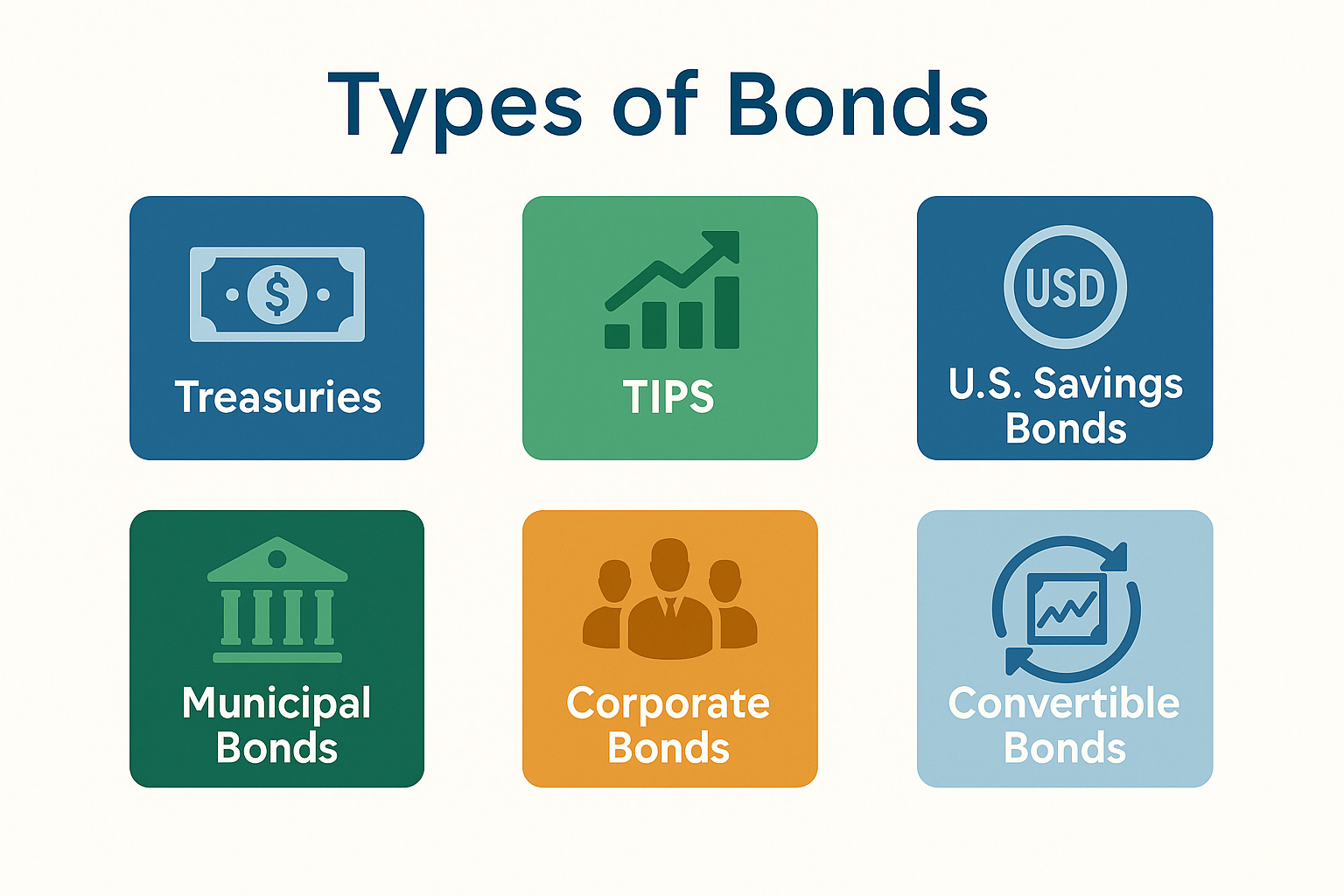

Types of Bonds

There isn’t just one kind of bond. Here are the most common categories investors should know:

1. Treasuries

Issued by the U.S. government and backed by its full faith and credit. They come in different maturities:

T-Bills – Less than 1 year. Sold at a discount, no coupon payments.

T-Notes – 2 to 10 years. Pay semiannual interest.

T-Bonds – 20 to 30 years. Long-term government debt.

2. TIPS (Treasury Inflation-Protected Securities)

The principal value adjusts with inflation (CPI). Coupon payments rise when inflation is high, protecting your purchasing power.

3. U.S. Savings Bonds

Series EE (fixed rate, guaranteed to double in 20 years) and I Bonds (inflation-adjusted) are accessible directly through TreasuryDirect.gov. Minimum investment: just $25.

4. Municipal Bonds (Munis)

Issued by state or local governments. Their big advantage? Interest is usually federal tax-free and sometimes state tax-free too. Popular with higher-income investors.

5. Corporate Bonds

Issued by companies. These carry credit risk — the chance the company defaults. Ratings matter:

Investment Grade: BBB- or higher. Safer, lower yields.

High Yield (Junk): Below BBB-. Higher yields but higher risk.

6. Callable Bonds

Allow the issuer to repay you early, usually when interest rates fall. Good for the company, less so for you.

7. Convertible Bonds

Start as bonds but can be converted into stock. They pay lower interest in exchange for stock-like upside potential.

8. Zero-Coupon Bonds

Don’t pay interest along the way. Instead, they’re sold at a discount and mature at full value. Popular for long-term goals like college funding.

Primary vs. Secondary Markets

When a bond is first issued, it’s sold in the primary market. Big institutions usually dominate here, buying in large blocks. Individual investors rarely get access.

Instead, most of us encounter bonds in the secondary market, where existing bonds are traded between investors. Like stocks, their prices fluctuate with supply, demand, and interest rates.

You can also buy bonds indirectly through mutual funds and ETFs, which offer diversification and easier trading.

Why Should You Care About Bonds?

Bonds may not have the drama of stocks, but they play three key roles in a portfolio:

Income: Reliable interest payments.

Stability: Less volatile than stocks, bonds can cushion downturns.

Diversification: They often move differently from equities, reducing overall risk.

Of course, bonds have downsides too — lower long-term returns and vulnerability to inflation and interest rate changes. But they can be an important component of a balanced strategy, particularly in or approaching retirement where volatility can hurt and where you are going to start living off the income from your investments.

Wrapping Up

So, what’s the bottom line? A bond is simply a loan — a way for issuers to raise money and for investors to earn income. The variety of bonds (Treasuries, munis, corporates, convertibles, and more) offers flexibility for different goals and risk tolerances.

In my next article, I’ll cover bond pricing including why bond prices fall when interest rates rise. Understanding that dynamic is critical for managing your portfolio.

And if you’d like a deeper dive into financial principles like bonds, stocks, and investing strategies, check out my book The Physician’s Path to True Wealth. You can also read the full companion article about bonds on my blog at www.bryanjepson.com