Three Foundational Financial Decisions for Physicians That Matter More Than Choosing the Right Index Fund

[This article was originally published on my website at www.bryanjepson.com. Check it out for more personal finance content including blog posts, videos and podcast appearances.]

Physicians tend to be detail-oriented and data-driven folks. You have to be if you want to be a great clinician, surgeon, or medical researcher. And, in my experience, that mindset often spills over into their investing style, especially for those who enjoy doing it themselves. Paying attention to those details is important, absolutely. It can save a lot of money over the long run. But it is also surprising to me how often DIYers might miss the forest for the trees.

This article is about prioritizing the things that matter the most in the long-term when you are building your financial plan. And, spoiler alert, it is not whether you choose VOO (an S&P 500 index) or VTI (a total US stock market index) as the primary investment in your portfolio.

Rather, true wealth, which I define as the ability to gain full control over how you spend your time coupled with the resources to maximize it, is usually built (or lost) through key early foundational decisions:

When you start investing

How much house you buy and when

How quickly you let lifestyle inflation take over

Your specialty and how long you choose to work

Why Big Financial Decisions Matter More Than Investment Selection for Physicians

Fresh out of residency, it feels like you have your whole career ahead of you. Finally, you are starting to make real money. But there are a lot of competing interests vying for that new discretionary income. Retirement seems like a very long way away with lots of paychecks between now and then to make up for any suboptimal financial choices, right?

It is very tempting to spend a little more now than you had originally planned--to buy a bigger house, drive a nicer car, or go on more vacations. It is even tempting to put off saving for your retirement to do something that sounds very fiscally responsible: pay off student debt early.

The problem isn’t that any of those things are inherently bad, it is that those choices now may impact your freedom to make equally important choices later on.

Let’s talk about a few of these decisions and run some numbers to show what I mean.

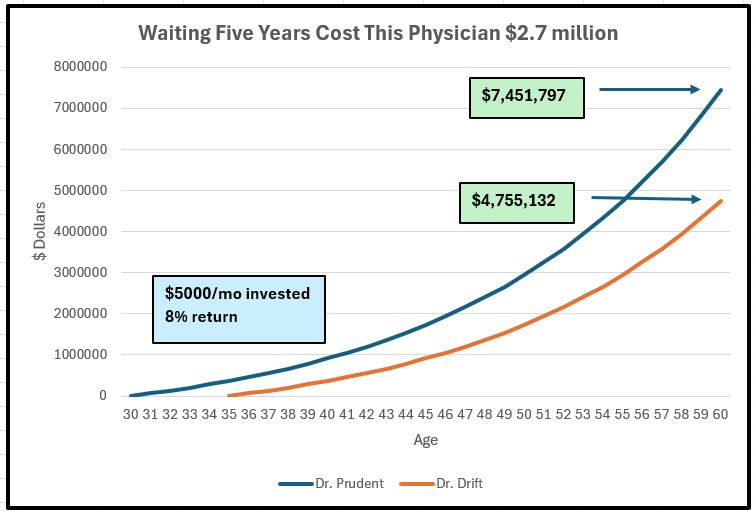

Decision #1: Delaying Investing by Five Years

Let’s look at how just a 5-year delay will impact the size of your portfolio when you are ready to retire.

Here is the case of two physicians, Dr. Prudent and Dr. Drift:

Dr. Prudent starts investing at age 30, as soon as he is out of residency.

Dr. Drift starts investing at age 35, 5 years into his attending career.

Both invest:

$5,000/month

Both retire at age 60

Assume:

8% annual return

And here is the result:

Five years doesn’t feel like much at first. Yet those years outside of the market cost Dr. Drift $2.7 million! And that difference becomes even more profound if they both decide to wait until age 65 to retire. At that point, the difference is over $4 million!

Teaching points:

Time in the market matters. The power of compounding interest means that our investments grow exponentially. But you need time before you reach the steeper part of the growth curve. Once it hits though, it feels like your asset growth is riding a rocket. Early investing is like building a more powerful booster engine!

Plus, this chart is just a simple time value of money comparison. It doesn’t account for the cumulative savings from deferring taxes during your high-income years or the added growth from an employer’s match.

Another point to remember: “time in” the market is more important than “timing” the market. The best time to invest is now—even if the market is at an all-time high. Trying to figure out if it is going to drop before jumping in and by how much is a fool’s errand. It is just as likely to go up as it is to go down. Or even if it does drop, market recovery typically happens in short bursts, and if you are not invested during those particular good days, you miss out on a lot of the long-term growth. It is best to just get in and let the market do its thing, especially if you have a long time horizon.

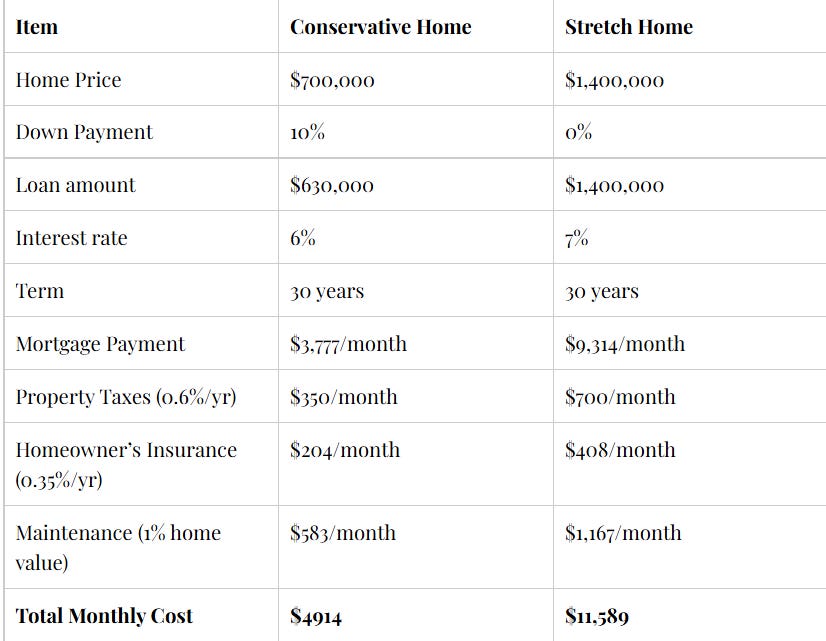

Decision #2: Buying Too Much House

You have been stuck in a lousy apartment for all your adult life so far while getting through medical school, residency and maybe even a fellowship. Now that you are an attending, you can’t wait to spread your wings and stretch your legs. Plus, real estate is always a great investment, right?

The answer to that is no, not always. Let’s look at another scenario:

Dr. Prudent buys a $700,000 home—still a major upgrade from where he has been living. He had saved up for a 10% down payment.

Dr. Drift buys as much home as the no-money down doctor loan would allow: $1.4M

The difference? $6,675 per month! That’s over $80,000 per year. Now, invest that difference instead for 30 years at 8%? $9.95 million!! Wow! And we didn’t even account for the cost of furnishing that new, expensive home.

The story gets sadder. After Dr. Drift had been at his first job for the first year, he discovered that it wasn’t at all what he was sold. He worked crappy hours, failed to live up to unrealistic productivity expectations, and did not get paid what he anticipated. Plus, he hated the area and wished that he would have just taken that less sexy but much more comfortable position in his hometown.

The problem? He now had a house that he had to sell. Oh, and the local housing market dropped in value over the last year by 3%. Because he used a no-money down loan, he was now underwater on his mortgage.

So, what was it going to cost him to get out of this bad decision? 6% in real estate fees to start with. The home was now valued at $1.36 million. So, the realtors will pocket $81k. And after one year, he has barely made a dent in the principal and still owes $1,385,800. Add that up and it will cost him over $100k just to get out of the property. Not to mention moving costs. With an attending physician lifestyle to support, he didn’t have that kind of cash available. So he is stuck in a job that he hates, merely because of a bad real estate decision.

Teaching points:

Housing is often the biggest financial decision physicians make. Choose wisely. Not just the size but also the timing. I think it is better to rent for the first few years into your first job to be sure that you are happy with it. Nearly 60% of physicians leave their first job within 3 years!

Renting will also give you a chance to learn more about the area and figure out exactly where you want to live long-term. And then, be conservative with your first house. You can upgrade from apartment-living, but you don’t need a mansion. Invest that extra money in your retirement accounts instead.

Decision #3: Early Lifestyle Inflation

Physicians-in-training are the masters of delayed gratification, right? While our friends from high school got jobs straight out of college and seem so far ahead of us financially, we are still slaving away in the hospital at less-than-minimum wage if calculated by the hour.

What gets us through those late nights and early mornings? Sometimes it is dreaming of what our financial lives are going to look like when all our training is behind us. That is when our less educated or lower-compensated friends are going to be jealous, right? When we see the sudden increase in numbers in front of the decimal on that first paycheck, we are ready to make our dreams come true.

Well, let’s run another scenario:

Dr. Prudent increases monthly spending after residency by $3000 per month—still a pretty nice lifestyle bump. That equates to better housing, a reliable car, a reasonable travel budget, and some breathing room.

Dr. Drift bumps spending by $6000 per month. He figured that was achievable based on his new attending salary. That means bigger house, nicer cars, sweeter vacations, and even a club membership.

The difference in annual discretionary spending between the two? $36,000 per year.

If that difference in lifestyle is sustained into retirement and you use the 4% rule, Dr. Drift would need $900,000 more invested to sustain it. Think about it this way: for every $3000 extra a month in spending, you need nearly $1 million extra saved in your retirement account.

Or let’s frame it a little differently, where it will really hit home. If you are making $350k per year and your savings rate is 20%, you are saving $70,000 per year. If you invest it and it grows at 8% per year, that is 8.7 more years of work to accumulate that extra $1 million.

Teaching points

Relatively small recurring spending changes create massive retirement implications.

Lifestyle inflation is often invisible because it happens gradually. And once you reach a certain lifestyle, it is very difficult to reverse it if you need to. Rather, it tends to continue to creep upward over time. So, it is much better to build into it purposefully and only after you have some other financial ducks in a row. Then you can give yourself permission to spend more, realizing that your nest egg can support it.

Financial independence is more often delayed by consumption, not poor investing.

Creating True Wealth Through Financial Structure

Hopefully the above three examples are illustrative of how early career lifestyle decisions have an oversized impact on the quality and timing of your retirement years. Smart choices help you regain control over your time because you now have the financial resources to get to choose how you want to live.

Perhaps that choice is to keep working in some form—not because you have to, but because you enjoy it, and it adds value to your life. Extending your working life by even a few years can also have a large effect on your nest egg. Not only does it delay the draw down, but it allows you to keep saving and watching it grow during those peak exponential growth years.

If you are wealthy, you can likely structure your work life to be much more aligned with your values, because you have the extra negotiating power of saying “no” and to just walk away. This makes work a lot more enjoyable and might mean that you want to keep doing it for longer.

The Bottom Line: Build the Foundation Before You Optimize

DIY investor physicians may spend hours at the water cooler debating the value of VOO over VTI as a core holding, or vice versa. The reality is that the long-term difference between them is 0.2 to 0.5%. Same goes for which index funds have the lowest expense ratios. Or how much they are paying their fee-only financial advisor. And those decisions can definitely compound over time. But if you don’t create the discipline to get that money in your investment accounts in the first place, those details won’t matter much.

Pay attention to those things, absolutely. Every little bit can have an impact when talking about compounding over 30+ years. But remember, creating true wealth does not require you to find that perfect investment. It is much more about building a financial structure on a solid foundation that will ultimately help you create a life where you have true control over your time, your work, and the way you choose to live.

If you would like help building that kind of structure for your own finances, reach out to me at bryan@targetedwealthsolutions.com.

Disclaimer: the material in this blog post is intended for general educational purposes only and should not be considered specific financial advice. You should always consult with your personal financial advisor to see how it might fit within your personalized financial plan.